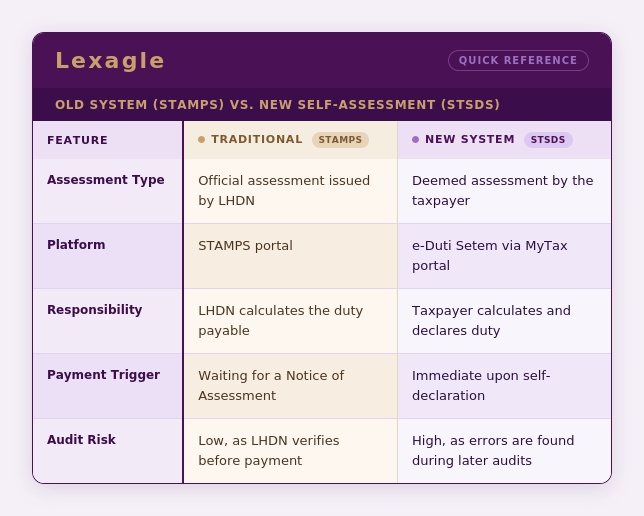

Starting 1 January 2026, Malaysia is adopting the Stamp Duty Self-Assessment System (STSDS). This change requires businesses to calculate, declare, and pay duty through the e-Duti Setem module on MyTax, replacing the old STAMPS portal. Taxpayers now hold the legal burden for accuracy because the Inland Revenue Board (LHDN) will no longer issue prior assessments. While a one-year penalty waiver applies to 2026 errors, companies must still meet the strict seven-year record retention requirement for future audits.

Why is the Shift to STSDS a Major Compliance Risk for Malaysian Enterprises?

The introduction of STSDS changes more than the way stamp duty is submitted. It fundamentally changes how compliance is managed within an organisation. Instead of relying on an official assessment before payment, businesses are expected to determine the correct duty themselves and retain sufficient evidence to support their decisions if questions arise later.

This creates a higher degree of taxpayer liability, particularly for organisations that manage large numbers of contracts across different business functions. An incorrect interpretation of the Stamp Act 1949, a misclassification of an instrument, or an overlooked deadline may not be identified immediately. In some cases, issues may only surface during an LHDN audit years after the original transaction was completed.

The challenge is particularly relevant for organisations handling high volumes of agreements. HR teams process employment contracts and renewals, procurement departments oversee supplier and service agreements, while property and facilities teams manage lease arrangements and tenancy renewals. Once a document is executed, the compliance timeline begins, creating a narrower window for assessment, approval, and payment.

From Official Assessment to Deemed Assessment

A key feature of the new framework is the move towards deemed assessment. Rather than waiting for LHDN to calculate the duty payable, businesses effectively make that determination themselves through the submission process.

As a result, organisations need more than basic administrative procedures. They require consistent assessment methodologies, clear approval processes, and documented reasoning that can withstand regulatory scrutiny. Legislative changes associated with the self-assessment regime, including provisions linked to Section 47A, further reinforce the importance of supporting documents and defensible compliance practices.

The Three-Phase Rollout of STSDS

The transition to self-assessment will be introduced gradually through a three-phase implementation plan.

Phase 1: 2026

The first phase covers tenancy and lease agreements, as well as security-related instruments. Because these are among the most common commercial documents used by businesses, many organisations will encounter self-assessment obligations from the beginning of the rollout.

Phase 2: 2027

The second phase expands the regime to include property-related transactions, including Instruments of Transfer. Businesses involved in real estate transactions will need to manage additional assessment and reporting responsibilities under the new framework.

Phase 3: 2028

The final phase extends self-assessment to all remaining stampable instruments governed by the Stamp Act 1949, completing the transition across Malaysia's stamp duty system.

Although the phased approach provides businesses with time to adapt, organisations should begin reviewing their processes early rather than waiting until their instruments become subject to self-assessment requirements.

Why Manual Tracking Creates Audit Risk

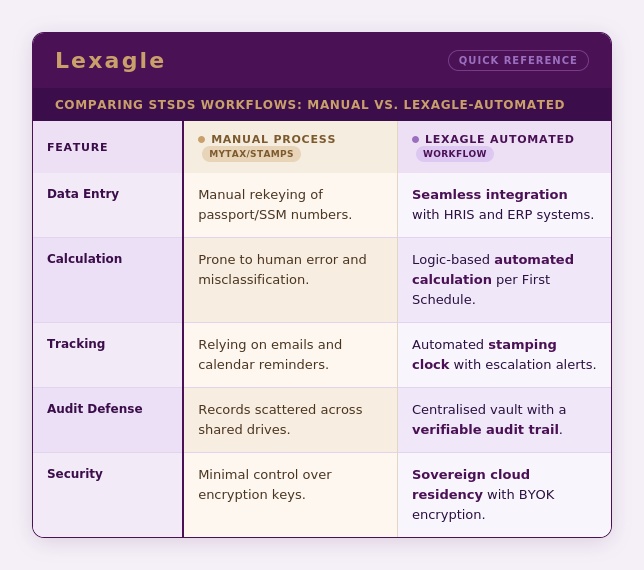

Many organisations continue to monitor stamp duty obligations through spreadsheets, email chains, and shared folders. While these methods may have been workable under the previous model, they become increasingly difficult to support in a self-assessment environment.

When a duty assessment is reviewed, organisations may need to demonstrate how the amount was calculated, which provisions of the Stamp Act 1949 were applied, who approved the assessment, and when payment was made. Retrieving this information can be challenging when records are spread across multiple systems or departments.

The challenge extends beyond calculation accuracy. Businesses must also satisfy Malaysia's seven-year tax record retention requirements by preserving contracts, supporting calculations, payment confirmations, and stamp certificates in an accessible format.

Organisations that establish structured assessment procedures, documented approval workflows, and reliable recordkeeping practices early will be better positioned to respond to regulatory reviews and maintain ongoing compliance.

How Do You Calculate Stamp Duty Malaysia Under the First Schedule?

Accurate stamp duty calculation sits at the heart of the STSDS framework. As businesses take responsibility for assessing duties themselves, understanding how different instruments are treated under the First Schedule of the Stamp Act 1949 becomes essential.

The amount payable generally depends on whether an instrument attracts Ad Valorem Duty or Fixed Duty. Identifying the correct category is the first step in determining the applicable duty and avoiding assessment errors.

Ad Valorem Duty vs Fixed Duty

The distinction between Ad Valorem Duty and Fixed Duty forms the basis of most stamp duty assessments in Malaysia.

Ad Valorem Duty is calculated as a percentage of a transaction's value. The duty payable changes depending on factors such as the loan amount, rental value, consideration paid, or other prescribed measures.

Fixed Duty applies a predetermined amount regardless of transaction value. As long as the instrument satisfies the relevant legal requirements, the duty remains unchanged.

Employment agreements are among the most common instruments assessed by HR teams. Under Item 4 of the First Schedule, employment contracts that establish a genuine master-servant relationship generally attract a fixed RM10 duty. The amount remains the same regardless of salary level, benefits package, or contract value.

Loan agreements and security instruments are typically subject to Ad Valorem Duty. In many cases, the applicable rate is 0.5% of the loan amount or secured value, although the exact treatment depends on the nature of the transaction and any available exemptions, remissions, or reliefs. Because financing arrangements often involve substantial values, even small assessment errors can create significant duty shortfalls.

Tenancy and lease agreements, which form part of the first phase of the STSDS rollout, are assessed differently. Duty is generally determined by factors such as annual rental value, whether annual rent exceeds RM2,400, the duration of the tenancy, and the applicable provisions within the First Schedule. Longer lease periods generally result in higher duty obligations because the assessment reflects the value of the arrangement over time.

Why Accurate Classification Matters

The move to self-assessment places greater emphasis on consistency and documentation. Businesses can no longer rely on a pre-payment review by LHDN to identify classification errors before duty is paid.

This makes First Schedule compliance a practical business requirement rather than a purely administrative exercise. Establishing consistent assessment procedures helps organisations apply duty rules more accurately, reduce unnecessary disputes, and manage growing compliance obligations more efficiently as additional instrument categories enter the STSDS regime.

What are the LHDN Stamping Penalties for Late Payment in 2026?

Calculating the correct duty is only part of the compliance process. Businesses must also ensure that instruments are stamped and paid within the statutory timeframe.

Under Malaysia's stamp duty framework, most instruments must be stamped within 30 days of execution in Malaysia. Missing this deadline can result in penalties even if the underlying duty is eventually paid.

What Happens if You Miss the 30-Day Stamping Deadline?

Effective from 1 January 2025, LHDN applies a revised penalty structure for instruments that are not stamped within the prescribed period.

For delays of up to three months after the deadline, the penalty is RM50 or 10% of the deficient duty, whichever is higher.

For delays exceeding three months, the penalty increases to RM100 or 20% of the deficient duty, whichever is higher.

These amounts are payable in addition to the original stamp duty obligation. While the penalties may appear modest on individual transactions, the financial impact can increase quickly when multiple agreements are involved.

Don’t let a missed deadline lead to a 20% penalty. Lexagle’s automated "stamping clock" tracks your 30-day window from the moment a contract is executed. Protect Your Workflow Now

Incorrect Assessments Can Increase Penalty Exposure

Late stamping is not the only risk under the STSDS framework. If an organisation underpays duty because an instrument was incorrectly classified or assessed, LHDN may require payment of the deficient duty together with any applicable penalties.

For higher-value transactions, even a small assessment error can create a significant financial exposure. Meeting the deadline alone may not be sufficient if the original duty calculation cannot be supported.

Supporting Documentation Remains Essential

Organisations should retain executed agreements, assessment calculations, payment confirmations, and digital stamp certificates throughout the mandatory retention period. These records should be organised and readily accessible if requested during a compliance review.

As Malaysia moves towards a broader self-assessment environment, effective compliance depends on both accurate assessments and disciplined documentation practices. Businesses that establish structured processes for calculating, approving, and retaining duty records will be better positioned to manage future regulatory scrutiny and reduce exposure to late stamping penalties.

How does Lexagle Improve LHDN Compliance with STSDS?

The transition to the Sistem Taksir Sendiri Duti Setem (STSDS) changes stamp duty from an occasional administrative task into a front-line compliance workflow. To manage this shift effectively, enterprises must move away from fragmented processes where records are scattered across legal, HR, and finance departments.

By combining administrative preparation with digital automation, your organisation can transform STSDS from a liability into an operational advantage. Below is the actionable roadmap for mastering LHDN compliance using Lexagle’s integrated features.

1. Accurate Instrument Classification: Ad Valorem vs. Fixed Duty

- The Actionable Step: Businesses must immediately review their existing document templates—including tenancy and lease agreements, employment contracts, and security instruments—to ensure they are correctly classified under the First Schedule of the Stamp Act 1949.

- How Lexagle Helps: Lexagle’s stamping module uses structured metadata (such as transaction value, tenure, and instrument type) to perform automated stamp duty calculation. This eliminates "spreadsheet guesswork" and ensures consistent application of duty, whether it is a fixed RM10 duty for employment offers or a tiered ad valorem rate for complex loan facilities.

2. Statutory Timeline Management: The 30-Day Stamping Clock

- The Actionable Step: Under STSDS, the 30-day payment clock begins the moment a document is executed in Malaysia. Missing this window triggers automatic statutory penalties of up to 20% of the deficient duty.

- How Lexagle Helps: The platform triggers a digital "stamping clock" the moment a contract is signed using legally recognised digital signatures in Malaysia. The system sends automated alerts to responsible stakeholders and surfaces pending obligations on a real-time dashboard to prevent any late-payment penalties.

3. Internal Governance: Role-Based Approval Matrices

- The Actionable Step: Organisations must define clear internal controls over who is authorised to assess duty, file the BNDS submission, and approve payments through the MyTax portal.

- How Lexagle Helps: Lexagle enforces role-based approvals aligned with your organisation’s specific matrix of authority. Routine agreements can follow streamlined paths, while high-value security or property documents are automatically routed to senior legal or finance leads for secondary review.

4. Long-Term Audit Readiness: The 7-Year Defense Strategy

- The Actionable Step: LHDN compliance requires businesses to maintain all stamped instruments and supporting records for a mandatory seven-year retention period to facilitate potential audits.

- How Lexagle Helps: Every action—from drafting to payment confirmation—is captured in a verifiable, timestamped audit trail. All digital stamp certificates, BNDS filings, and receipts are stored in a centralised compliance repository. To meet board-level security standards, all data is hosted within Malaysian jurisdiction using BYOK (Bring Your Own Key) encryption.

Strategic Insight: Maximising the 2026 LHDN Concession Period

To support businesses during the initial transition, LHDN has implemented a special educational concession from 1 January 2026 to 31 December 2026. During this phase, LHDN will waive penalties for incorrect or incomplete information submitted on the BNDS form under Phase 1.

How to leverage this with Lexagle: Use this one-year grace period to phase out risky manual spreadsheets. By implementing Lexagle now, your teams can refine their automated workflows and establish a sustainable compliance framework before strict enforcement begins in 2027.

Schedule Your 15-Minute STSDS Workflow Walkthrough. Stop the guesswork and protect your enterprise from high statutory penalties. Request a personalised demo today to see how Lexagle's automated calculations and audit-ready repository provide a total compliance advantage.

Transition to Stress-Free Stamping Today

STSDS changes stamp duty from an administrative obligation into an ongoing compliance responsibility. As businesses take on greater responsibility for assessment, filing, documentation, and retention, the limitations of manual processes become increasingly apparent.

As contract volumes grow, spreadsheets, email chains, and disconnected systems can create unnecessary compliance risks. A missed deadline, incomplete record, or incorrect assessment may lead to penalties, reassessments, and additional administrative costs.

Lexagle provides a secure, automated platform that supports the entire stamping workflow, from automated stamp duty calculation through to the management of digital stamp certificates and supporting compliance records. By embedding compliance activities directly into the contract lifecycle, businesses can manage obligations more efficiently while maintaining stronger oversight of their processes.

With automated workflows, deadline monitoring, centralised record management, and enterprise-grade security controls, Lexagle helps organisations maintain LHDN compliance while reducing the burden associated with manual administration.

Stop the spreadsheet guesswork and strengthen your seven-year audit defence with a platform designed for the STSDS era.

Use the 2026 grace period to phase out manual spreadsheets and build a bulletproof compliance framework before strict enforcement begins in 2027. These things are what Lexagle can do, book a demo now!